RBA preview: Softer underlying inflation favoring status quo in August with hawkish tone

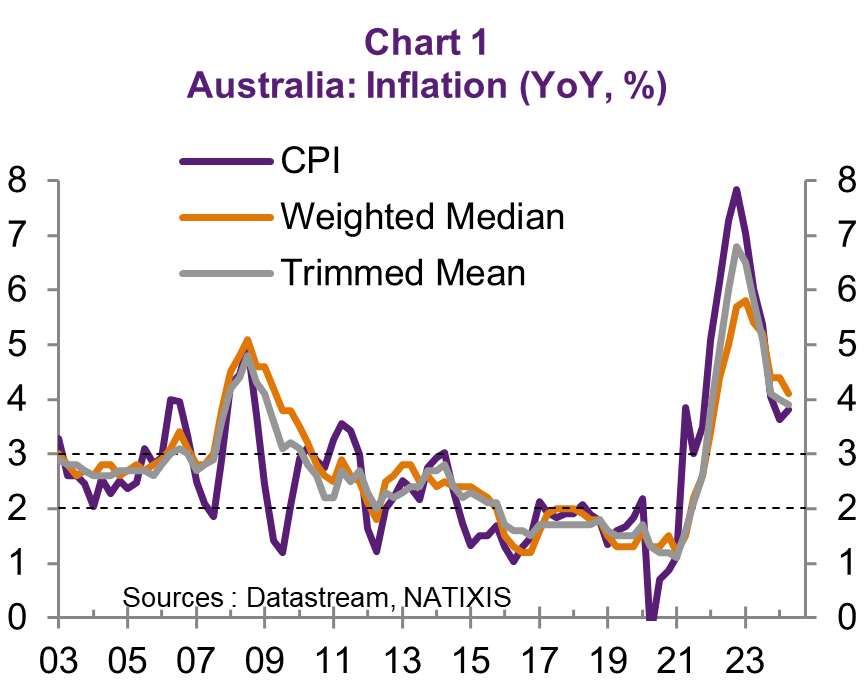

The Reserve Bank of Australia (RBA) must have been relieved to see the 425-bps rate hike from 2022 has been stabilizing inflation. Although the headline CPI picked up to +3.8% YoY in Q2-24, the underlying inflation measured by trimmed mean and weighted median both continued to decelerate (Chart 1).

With softer underlying inflation pressure, we expect the Reserve Bank to keep the cash rate stable. In fact, the cycle of rate hikes has brought about a surge in mortgage payments to about 10.5% of household disposable income. The eroding impact on consumers’ purchasing power has weakened real retail sales once again by -0.6% YoY in Q2-24 with consumer confidence remaining low (Chart 2). Furthermore, the labor market has been gradually cooling. While the unemployment rate rose to 4.1% in June, job vacancies, a leading indicator for employment, dropped once again by -18.1% YoY in June.

Nevertheless, the RBA will not have the urgency to ease in August. The Aussie has depreciated by 4.4% year to date, as the Fed has been cautious to ease on the back of a resilient US economy. These developments lifted inflation of tradables, which is sensitive to international trade, to +1.5% YoY in Q2-24 from +0.9% YoY in Q1-24, while non-tradables were flat at +5.0% YoY. Hence, a rate cut could further weaken the Aussie, which could in turn lift the headline inflation.

Therefore, after considering the risks of a rate hike on growth and a rate cut on inflation, the RBA is expected to keep the status quo in August by keeping a hawkish stance to contain inflation expectations.

*If you are interested in getting full report, please feel free to contact me.