US tariffs on China and friend-shoring policies to benefit the rest of Asia, especially Korea

US tariffs on China and friend-shoring policies to benefit the rest of Asia, especially Korea

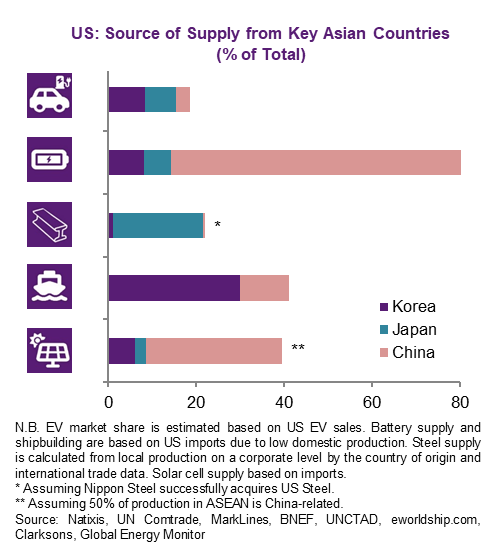

The latest import tariffs by US President Biden on Chinese green tech have confirmed the trend of trade protectionism, fortifying the US quest for friend shoring and industrial policies. While greater supply chain reshuffling can result in higher costs, the government-led changes and corporate-driven diversification rush may bring some winning sectors and firms in Asia. Our analysis of the new import tariffs and the potential Section 301 investigations show Asia’s corporate alternatives in electric vehicles (EVs), batteries, steel, shipbuilding, and solar panels will be the beneficiaries.

EVs and batteries: Korea and Japan are clearly alternatives

Regarding EVs, Korea and Japan accounted for 15% of US EV supply versus 3% from China in 2023. Korean EV producers increased their market share in the US from 4.3% in 2020 to 8.3% in 2023. For Japan, it depends on if consumers will prefer plug-in hybrid EV (PHEV), a mix of battery-powered electric motor and gasoline engine. On lithium batteries, 70% of US imports come from China, which means that there is ample room for other exporters to gain if they manage to have enough supply. Again, Korea and Japan are major battery makers globally and natural replacement choices, especially as they have 49% and 16% market shares respectively in non-China markets.

Steel: Opportunities from IRA beyond tariffs on China

Steel is another price-competitive product with additional tariffs. The opportunities hinge on if Asia’s steelmakers can enter the US market historically shielded by protectionism. The 100% domestic content rule on steel in green tech infrastructure means Asia’s steelmakers must produce in the US to capture the incentives. One example is Nippon Steel's move to acquire US steel, making it the third largest global steelmaker with its US revenue rising from 5% to 23% of total. Despite the political uncertainties, one should expect the US to prefer a Japanese firm entering its market to upgrade its steel industry than to have China pushing down prices globally. India could also benefit if the US were to reach a trade deal, thereby easing import duties.

Shipbuilding: Friend shoring and LNG demand to benefit Korea

As the US has just begun the Section 301 investigation on shipbuilding, the situation is now in full swing. After years of the shift of manufacturing gravity, China became the biggest shipbuilder with 50% of the global order book in 2023, followed by 31% by Korea and 10% by Japan. Currently, 30% of vessels purchased by the US come from Korea, mainly LNG carriers. The growing LNG exports from the US will also mean that it needs to order more ships, or the global traders must increase the fleet size, which will benefit Korea either way.

Solar cells: Asian firms with US investment will gain market access

Lastly, solar cell is a more complicated story as China supplies roughly 90% of the global demand, and many exports from China are re-routed to the US through third countries, prominently Malaysia, Vietnam, Cambodia, and Thailand. Korea emerges as an alternative in solar cells with a growing focus on the US. For example, Hanwha Solutions will produce 8.4 GW of capacity in the US, forming 75% of total capacity.

US protectionism on China to benefit the rest of Asia, especially Korea

The elevated geopolitical tension will create uncertainties in trade, but it will also present opportunities for sectors and companies in Asia. As a critical manufacturing hub, Asia will offer important alternatives as the US seeks supply chain security. This is particularly the case of Korea, followed by Japan. Some key countries in Southeast Asia will also benefit from China’s offshoring of production to avoid US tariffs. Still, there may be pullback in a scenario that the US scrutinize the source of products.

*If you are interested in getting full report, please feel free to contact me.