Is Hong Kong supporting the RMB?

Is Hong Kong supporting the RMB?

As China steps up its effort to internationalize the yuan, it will need to accept greater forex volatility and two-way capital flows, especially in the financial account. Using the concepts of foreign exchange receipts and settlements, we aim to provide a unique perspective on the capital flows in China's onshore market and Hong Kong. The latter now plays an increasingly significant role as a RMB offshore center. Amid the depreciation pressure, we analyze the implications of China’s capital flows in the financial account and the evolving role of Hong Kong on the yuan.

China experiences strongest net capital outflows pressure since 2015-17

Due to global monetary policy divergence and weak domestic sentiment, China faces a growing challenge in net capital outflows. On a trailing 12-month basis, there are net capital outflows of $139 billion in May 2024. The pressure is lower than $305 billion in 2016, but the difference is that the current account forex settlement is now in deficit. Together with the wanning foreign direct investment (FDI) and portfolio investment, China’s FX settlement ratio (how much conversion into the yuan for every dollar receipt) fell to 60% in May 2024 on a three-month average basis, the lowest since 2017.

Net capital outflows across the board

Looking into the financial account, China’s FDI inflows have plummeted as outward FDIs stays robust, leading to net capital outflows. Regarding portfolio investment, foreign investors have stepped up their Chinese bond holdings with a net increase of RMB 1.04 trillion ($143 billion) since September 2023. The major increase comes from negotiable certificates of deposits (NCDs), forming RMB 641 billion or 61% of total inflows, mainly for yield arbitrage opportunities with higher return than the US treasuries after swap arrangements. On equities, there are persisting net capital outflows through the Stock Connects. Compared to direct investment, the difference is China has tried harder to balance the capital flows of portfolio investment, such as the window guidance on Southbound bond connect.

Hong Kong is playing a greater role in RMB forex transactions

Although the last episode of capital flows in 2015 has dampened Hong Kong’s role as an RMB international center, there is improvement recently. From the asset perspective, Hong Kong is tiny compared to the overall RMB capital pool (0.5% of loan, 0.4% of deposits and 0.2% of bonds of the onshore market). However, it plays a significant role in the forex market with the turnover standing at 1.6 times higher than Mainland China as of April 2022, driven by FX swaps and spot transactions. Some latest data points also suggest Hong Kong’s overall RMB forex turnover expanding 22% further between April 2022 and October 2023. Conversely, the onshore total forex turnover (mainly RMB) fell 15%, reflecting the importance of Hong Kong.

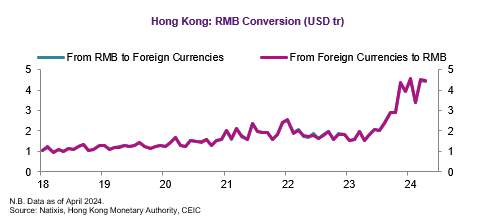

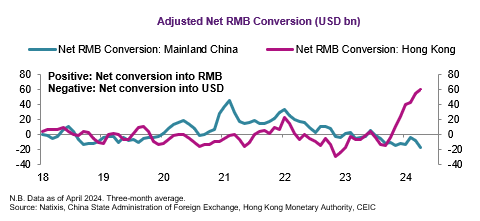

The direct implication is the net RMB conversion in Hong Kong will be as crucial as the FX settlement in the onshore market. Hong Kong handled almost $9 trillion of two-way RMB conversions per month in April 2024, 2.5 times the average level of 2020-22. On the one hand, the amount of RMB conversion into foreign currencies have ballooned possibly due to capital outflows. On the other, the conversion from foreign currencies into the RMB has grown even more with a net positive conversion of $60 billion in April 2024, higher than -18 $billion in the onshore market. In other words, Hong Kong offers a major net demand of RMB compared to mainland China.

Still, it is uncertain where the money comes from and goes. With the massive net conversion, RMB deposits in Hong Kong has barely increased, or at least not on the same scale. RMB remittances from Hong Kong to mainland China have multiplied, but it is several times larger than cross-border yuan trade settlement. It is also not reflected in the RMB receipts in the onshore market, which mainly includes corporates. This hints to the possibility of potential intervention to support the RMB but how this might be done is still a question mark with the information available.

Conclusion: Potential intervention flying under the radar?

Due to the challenges in economic growth, global monetary policy divergence and geopolitics, the RMB is facing possibly the strongest headwind since 2015-17. Against such backdrop, Hong Kong emerges as a venue to support RMB internationalization with a new twist in the large net positive conversion from foreign currencies into the CNH. Whether Hong Kong is becoming part of an unconventional toolbox to support the RMB is an open question which requires more analysis. What is certain is that the role of Hong Kong as a RMB center has made it an important center for yuan conversion, which is now supporting the currency in the offshore market.

*If you are interested in getting full report, please feel free to contact me.