Bank of Japan to pause with a hawkish rhetoric amid high market volatility

Bank of Japan to pause with a hawkish rhetoric amid high market volatility

Despite of the surging market volatility after the surprise rate hike in July, the Bank of Japan (BoJ) has kept its hawkish rhetoric. BoJ Board member Tamura said on September 12th at a conference in Okayama that the policy interest rate needs to be raised to at least 1% by FY26 to avoid upside risks on inflation. Financial markets immediately responded with a stronger Yen and drop in equity prices to his hawkish comments.

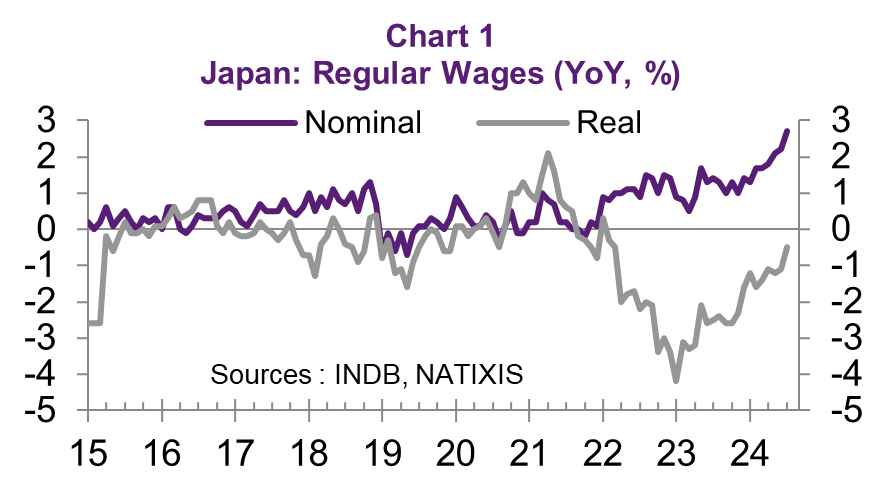

In fact, the virtuous circle between nominal wages and inflation has gained momentum as the decline in real wages has been shrinking (Chart 1). While the core CPI has been above the BoJ’s 2% inflation target since April-22, nominal regular wages accelerated to +2.7% YoY in July, the highest increase since 1992, after the successful spring wage negotiation. Furthermore, the government’s decision to reintroduce the energy subsidy for three months in August should give additional respite to real wages, supporting a BoJ hike.

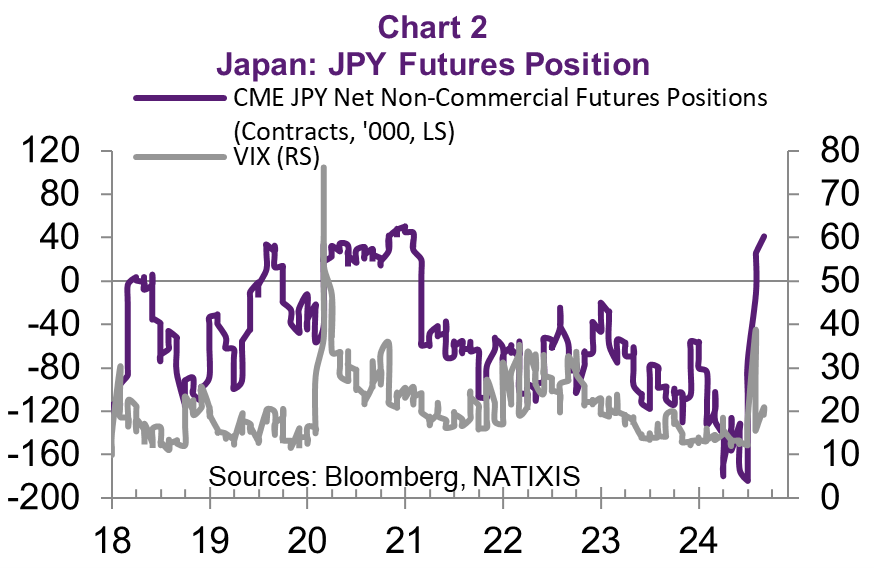

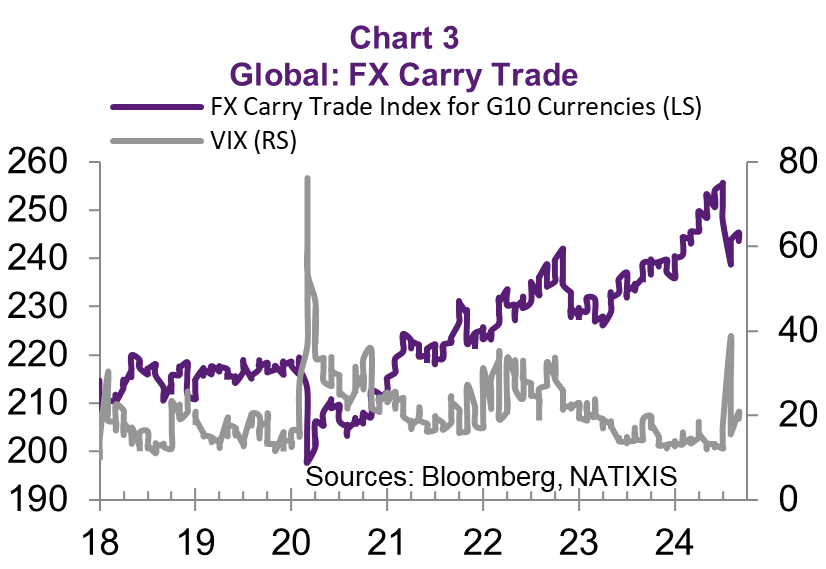

At the same time, the window for a rate hike could be closing rapidly. On the back of a slowing US economy, the Fed is expected to initiate an easing cycle with a 225-bps rate cut by the end of 2025, which should support flows into Japan and further unwinding of carry trade positions. As speculative short positions in Yen futures have been closed rapidly, a rate hike could potentially trigger another avalanche of unwinding of carry trades, when market uncertainties remain relatively high (Chart 2). As the Governor acknowledged at the Parliament the instability of the financial markets following the surprise hike at the July meeting, the BoJ will be very careful if the unwinding of carry trade positions accelerated in the run up to this BoJ meetings or following ones. Carry trade positions seems to be unwinding again, at least based on the Bloomberg FX carry trade index, which measures the total return of the position (Chart 3).

All in all, one could argue that September provides a sweet spot for the BoJ to hike as the pressure might be less (as the market reviews Fed cuts to only 25bp in September) but the Yen continuous appreciation is putting pressure on the BoJ to be careful. Given how close in the memories of early August’s Black Monday must be, we expect the BoJ to wait for one-two months to calm the waters before hiking again.

*If you are interested in getting full report, please feel free to contact me.